Too Conservative is Risky

/Yes, you read that correctly – being too conservative can be risky.

Risk of what? Loss of value. Although volatility of financial securities is a reality, the loss of value is different. Ups-and-downs of security market prices happen, known as volatility, and is reflected mathematically as standard deviation. These statistics are helpful measures for evaluating relative risk-adjusted returns over time. However, the absolute risk of loss of value is when negative volatility (periods when prices are down) is made permanent.

Permanent loss can be from either a bad investment or when an investor panics and sells a security when it is down out of fear of it going down further. One may think they’re being conservative, but over time may be proven wrong. If a fundamental investment thesis of the underlying stock, for example, remains intact, then normal volatility is to be expected. A stock may be relatively risky as observed through its peaks and troughs; however, a good fundamental investment in the equity of a company is expected to have gains over time.

We often quote Brian Wesbury of First Trust, and we attribute this quote to Brian as well, “Volatility is the price we pay for gains over time.” It doesn’t feel good in the moment, but moving through volatility pays off over time. Investors need to maintain their rebalancing discipline which is critical to long term wealth management objective achievement.

Permanent loss of value on an absolute basis is concerning; and, in a counter-intuitive manner, being too conservative can be risky, and this is the environment in which we currently live. There are two areas for which I’ll reference – cash & high-quality bonds. These two asset classes are typically thought of as ‘safe haven’ investments, but have their own risk considerations.

Cash is a critical component of any individual’s total financial picture. It provides immediate relief through the liquidity afforded during a crisis. In an emergency, “Cash is King” as the saying goes. Cash and cash equivalents can be a good non-correlating asset to stocks through sound portfolio management based on the principles of modern portfolio theory.

What is being highlighted here is the hoarding of cash out of fear. Cash held above and beyond both emergency purposes and designated for a specific purpose is unhealthy and can be risky. Cash loses value against inflation when its interest payment is less than the inflation rate (which it is today). The higher the rate of inflation, the greater the diminishment of purchasing power in the future. The irony is that one invests to grow assets to stay ahead of inflation over the long term in a desire to meet future objectives. Therefore, the hoarding of cash counteracts the very intention of investing by locking in losses in ‘Real Terms’ and thereby undermining intentions through the hoarding of cash.

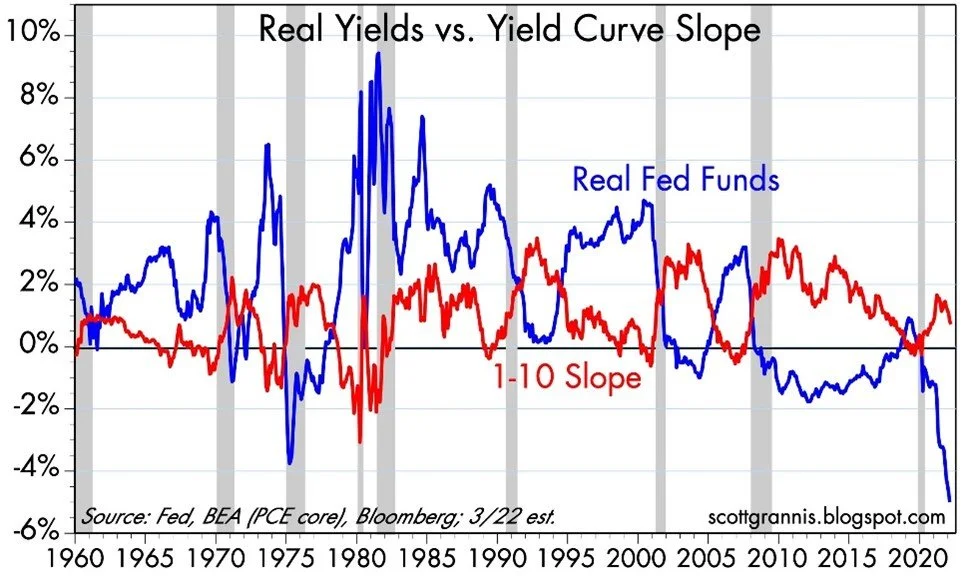

The Real Fed Funds Rate is at a historically negative level as calculated by the Fed Funds Rate minus the Rate of Inflation observed below. Said another way, if one wants to visualize the rate of return on excess cash in real terms it is approximately -5% (see the blue line in the below chart).

High Quality Bonds and interest rate risk. Clearwater Capital has written extensively about the concerns associated with the very low interest rate environment, Central Bank intervention (aka The Fed), inflationary pressures through the rapid increase of the M2 Money Supply through Fiscal Spending (aka Congress/President), and the inverse relationship between interest rates and bond values. In short, as interest rates rise (as they typically do in response to inflation) then bond values drop. The concept behind this calculation is called Duration which reflects the time-weighted value of cash flows associated with a bond. Duration indicates the level of interest rate sensitivity indicating how much a bond may drop in value with an associated rise in rates.

We previously communicated Inflation on All Fronts. The Federal Open Market Committee’s response associated with their dual mandate (full employment / stable prices) compels them to raise policy rates while markets are raising rates for longer duration bonds.

This year we have already witnessed some massive moves in interest rates upwards. Most news and headlines tend to reflect the volatility of the stock market. However, as I write on 3/31/2022, the 2022 year-to-date returns for U.S. stocks is being down 2-4% for the Dow Jones Industrial Average and S&P500 with smaller companies (Russell 2000) and tech heavy NASDAQ down approximately 6-8%. It has been negative stock market volatility to start the year.

If investors thought that the Aggregate Bond market was going to be more conservative and safe, they may be surprised to learn both in the United States and Globally the Aggregate Bond Market indices are down 6-7%. The amount of interest being paid on those bonds just cannot keep up with the rapid rise in market rates (through the selling of bonds which drops the price) given the inflationary backdrop.

Some would argue that if you hold the bond to maturity and there is no default, you’ll receive the interest and your money back. This is true; however, if you invested in a 10-Year U.S. Treasury today with an interest yield of approximately 2.3%, then any inflation above that level means the investor is losing money over time (10 years in this example) on a ‘Real’ basis; i.e. less purchasing power overall. Additionally, that bond will experience volatility in price/value, so one must be prepared to hold for the full ten year term. Therefore, the buying and holding of individual bonds for long periods of time can be a risk unto itself.

Safe havens today may not be so safe as investors must process the multitude of considerations within their overall portfolio strategy.

In closing, yes, investors today can put themselves and their futures at risk by being too conservative.

John W. Sleeting

Executive Partner